Europe has invested billions in wind and solar power in recent years (IEA) with the promise of cleaner electricity and lower prices for consumers. Yet the reality is more complicated. In many European countries electricity prices remain high, and even nations with abundant renewable capacity sometimes fail to fully realise the economic and environmental benefits.

In regions like Central Western Europe (spanning Germany, France, Belgium, Luxembourg, and the Netherlands) electricity is traded through an integrated cross-border market. Prices are often set by the most expensive plant needed to meet demand across the entire coupled region, even when cheaper renewable generation is available locally. As a result, electricity can remain costly despite abundant wind or solar power, because the market price reflects the last, most expensive unit required rather than the average cost of generation.

The reason is not a lack of renewable generation but the way electricity systems are designed.

In the Netherlands, electricity from offshore wind farms is sent directly into the main high-voltage grid. This means it reaches the wholesale market and can help lower electricity prices. By contrast, most onshore wind is connected to regional electricity networks managed by distribution system operators, which handle the delivery of power to local homes and businesses. These smaller networks often experience congestion, constraining or curtailing output. As a result, renewable electricity that could displace largely imported fossil fuels is not fully utilised, while gas-fired plants, operating within the marginal pricing framework of the European electricity market and influenced by carbon costs under the EU Emissions Trading System, continue to set prices, weakening the overall impact of renewables.

Despite significant investments in wind power, substantial volumes of renewable electricity across Europe are curtailed each year due to grid constraints. In 2025 alone, Germany, France and the Netherlands curtailed a combined 3.9 TWh of renewable generation, highlighting how system limitations can prevent available clean energy from being used. This is a travesty.

The challenge is only set to intensify. Across Europe, rising electricity demand from industrial electrification, including hydrogen production, e-fuels, and data centres, is expected to place increasing strain on already constrained power grids, reinforcing the need for alternative off-grid or self-generation solutions. This dynamic is already visible at the national level; in Finland, for example, electricity demand is projected to grow from around 83 TWh today to approximately 123 TWh by 2030 (Fingrid), showing how rapidly expanding industrial loads are set to compound existing system bottlenecks.

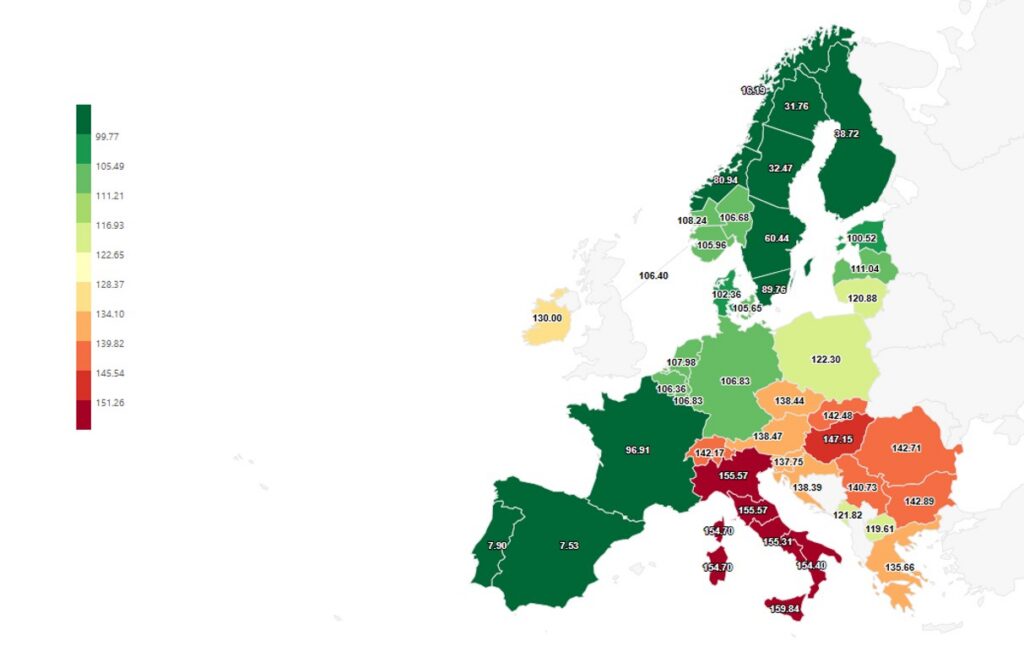

Spain offers a contrasting experience. Its electricity market is less tightly coupled with the rest of Europe, meaning that local renewable availability has a stronger effect on wholesale prices. At times in early 2026, wholesale day-ahead electricity prices in Spain fell to very low levels, for example around €7.5/MWh in one recent week, compared with prices in most of continental Europe, where many markets (including Germany and the Netherlands) were clustered around ~€95–€120/MWh on the same basis. This shows that Spain’s market, being less tightly linked to broader continental pricing and with high renewable output, can experience much lower wholesale prices than Germany and the Netherlands.

Average day-ahead electricity spot market prices in week 14 2026 in EUR/MWh:

This highlights the urgent need to modernise Europe’s energy systems. Yet transforming vast infrastructure originally designed for conventional generation to fully accommodate renewables will take considerable time.

“From my perspective,” says Elcogen CTO, Jan Gustav Grolig, “Europe faces several challenges in positioning itself to meet its renewable energy ambitions over the next decade, but there are also clear opportunities,” adding,

“One key issue is indeed the pace of grid build-out, which is currently lagging behind what is required to support large-scale renewable deployment. As a European, I sometimes find it frustrating that we do not fully recognise the strategic importance of energy. Although transitioning to a system with a higher share of renewables may be more complex, it ultimately creates a more resilient energy system. Such a system is less dependent on imports and less vulnerable to external threats, not only because of reduced reliance on foreign energy sources but also because generation is more decentralised and therefore less susceptible to targeted attacks”.

Why energy systems need more than electrons

This is where green hydrogen comes in. Produced by renewable-powered electrolysis (using renewable electricity to split water into hydrogen and oxygen), it offers a flexible solution for energy curtailment and market inefficiencies. While fast-ramping electrolysers (such as PEM) are particularly suited to responding to short-term grid congestion and volatility, hydrogen’s role in Europe’s energy system goes beyond simply absorbing excess power at constrained nodes, and should be seen as complementary to other flexibility options such as batteries and demand-side response.

One such complementary approach is to deploy electrolysers, including solid oxide electrolysers (SOEC), which operate most efficiently at steady high loads, in regions with structurally abundant and underutilised renewable energy, such as in the Nordics and Spain. In these areas, renewable generation often exceeds local demand or cannot be fully exported due to limited interconnection capacity. Rather than forcing all electricity through congested grids, converting it locally into hydrogen can be a more efficient system-level solution.

By converting renewable electricity into hydrogen, energy can be stored for later use, reducing waste and easing pressure on congested power networks. This “molecules over electrons” approach can, in specific cases, offer advantages over battery storage, particularly for large-scale and long-duration applications where batteries become costly and resource-intensive, while batteries remain more efficient and cost-effective for short-duration storage and fast grid balancing. Excess wind or solar generation can be converted into hydrogen and then stored, transported, or used directly in industry and transport, or reconverted into electricity when needed. Locating hydrogen production close to both renewable resources and industrial off-takers further reduces the need for some grid expansion.

In this way, green hydrogen acts as a flexible buffer that stabilises electricity supply, integrates renewables more effectively, and reduces reliance on fossil-fuel plants within the existing system, particularly over longer timeframes and in hard-to-electrify sectors.

This is also where technology differentiation becomes critical. Elcogen’s solid oxide platform is designed specifically for high-efficiency conversion in such conditions, where steady operation and system integration matter more than short-term responsiveness. There are two main points to consider here, states Grolig,

“First, Elcogen’s solid oxide technology is particularly well suited to industrial settings, such as steel mills or other industrial use cases, where heat streams can be effectively integrated and operational profiles align closely with the technology’s capabilities. These sites are often located in regions where electricity supply is constrained and expensive, which makes high conversion efficiency a clear advantage.”

“Secondly, when operated in solid oxide fuel cell (SOFC) mode, the same technology already provides a viable and efficient route for converting natural gas or hydrogen into electricity.”

Policy momentum and the build-out of Europe’s hydrogen economy

In March 2026, Germany took a big step toward a hydrogen-powered future. The Bundestag approved the Hydrogen Acceleration Act, designed to speed up the country’s hydrogen infrastructure. The law fast-tracks approvals for production, import, transport, and storage projects, while protecting them from legal hurdles. Officials say hydrogen will play a key role in hitting climate targets, ensuring a stable energy supply, offering low-carbon options for industry, transport, and heating, and helping balance renewable electricity. In the country, existing natural gas pipelines are being converted to transport hydrogen, forming a central north-south corridor and laying the foundation for a Europe-connected hydrogen core grid. This growing policy momentum reflects a broader shift in mindset.

While green hydrogen looks like the panacea on paper, there are significant challenges to be overcome, and subsidising the current high cost remains the primary one.

The cost and scale challenge facing green hydrogen

Today, green hydrogen in Europe typically costs around €5–€8/kg depending on electricity prices, utilisation and project design, compared with roughly €1–€2/kg for grey hydrogen (Grey hydrogen is produced by extracting hydrogen from natural gas using steam methane reforming, releasing carbon dioxide), while most analyses suggest it needs to fall to around €2–€3/kg to enable broad industrial substitution in sectors such as steelmaking (IEA, European Commission, Hydrogen Council), making access to low-cost renewable electricity and high utilisation rates critical to competitiveness.

There are also important technology-specific hurdles, shares Grolig, “Solid oxide technology has been around for a long time; however, particularly in electrolysis applications, it has not yet been proven at very large scale. As a result, the industry needs first movers who are willing to take on this challenge and demonstrate its viability at scale. At Elcogen, we have noticed an uptick in interest and are forecasting rapid uptake from 2030 onwards”.

Geopolitics is accelerating Europe’s hydrogen shift

Recent geopolitical tensions are sharpening Europe’s focus on building a domestic hydrogen economy. In response to the ongoing Strait of Hormuz crisis, the European Commission is reportedly preparing to bring forward its review of the bloc’s green hydrogen rules by two years, to as early as summer 2026. The move reflects growing concern that existing criteria for so-called renewable fuels of non-biological origin (RFNBOs), while designed to ensure environmental integrity, have inadvertently slowed project development and increased costs. By signalling a willingness to revisit these rules and accelerate the deployment of “clean, homegrown gases,” policymakers are acknowledging that hydrogen is not only a decarbonisation tool, but also a strategic asset for energy security and resilience. In today’s more volatile global energy landscape, the case for scaling domestic green hydrogen production is becoming as much about stability and sovereignty as it is about climate.

Other recent policy developments have underlined how seriously Europe is beginning to treat hydrogen as a structural solution rather than a niche technology. In March 2026, the European Commission approved a €440 million Spanish state aid scheme to support renewable hydrogen production under EU rules. The scheme will be implemented via the European Hydrogen Bank using its auctions as a service model.

The programme is expected to support up to 382 MW of electrolysis capacity and drive the production of around 243,800 tonnes of renewable hydrogen. The scheme provides direct subsidies per kilogram of hydrogen produced over a period of up to ten years, helping address one of the key barriers to scale which is cost competitiveness. It also supports Spain’s ambition to reach 12 GW of electrolyser capacity by 2030.

From a system perspective, this type of intervention reflects a growing recognition that hydrogen serves both to decarbonise end-use sectors and to address structural inefficiencies in Europe’s electricity system, particularly the mismatch between renewable generation and grid capacity, while complementing parallel investments in grids, storage, and flexibility.

Geopolitics is accelerating Europe’s hydrogen shift

“In practical terms,” states Grolig, “the most significant role for green hydrogen in Europe’s energy transition is replacing grey hydrogen, thereby driving industrial decarbonisation. This substitution can be done one-to-one, without requiring major changes to downstream processes”.

“The main deployment,” he continues, “will be in industrial sectors such as refining, green steel or ammonia production, especially, where hydrogen is already embedded in production chains and high-temperature requirements favour early adoption. Smaller-scale applications, for example in the glass industry and other niche uses, may also provide early footholds,” adding that,

“While electrolysers can respond dynamically, I see limited value in their use for grid balancing, per se, with their contribution likely remaining modest. More relevant is their potential role in seasonal energy storage via hydrogen derivatives, helping balance supply and demand over longer timeframes, while power-to-gas-to-power applications are likely a later-stage development once the technology has scaled”.

“Looking ahead, hydrogen use in power generation may develop further, but industrial demand will remain the priority. In future systems, solid oxide fuel cells could complement or partially replace conventional gas-fired generation, offering higher efficiency and lower emissions, though gas engines will likely retain advantages where rapid flexibility is needed.”

By converting otherwise curtailed renewable electricity into high-efficiency hydrogen through SOEC technology, Europe can unlock stranded clean power and reduce reliance on fossil-based hydrogen in industry, improving overall system efficiency and easing pressure on constrained parts of the electricity network, particularly in regions with persistent renewable surpluses rather than short-term congestion alone.

Text: Laura Quinton